1. 什么是ESPP(Employee Stock Purchase Plan)?

ESPP全名Employee Stock Purchase Plan,最常见的就是Section 423 ESPP ,是公司提供给员工的优惠认股计划。员工可以自行选择是否要Enroll、也可以决定要用多少税后薪资提拨(通常会设有上限金额&比例)。也因为是员工认股激励计划,公司通常会希望员工长期持久股票,股票持有越久可能代表员工对公司前景看好、也可能进一步稳定员工留在公司的时间。

通常公司通常会提供10%-15%的认股折扣给员工购买;有的还会有lookback period,也就是说会去看Purchase date跟往回看Offering date两个日期的股价、择其低者打8.5折/或9折(看公司提供的是10%还是15%折扣)。常见的ESPP Offering period是12个月。从Offering date开始起算、往后6个月是第一个购买时间点、第一个购买时间点再往后是第二个购买点。

2. ESPP购买时的税务问题

ESPP购买时是公司提供折扣价、但员工是用自己的After-tax money购买,所以购买时不会有税务议题,公司自然也不用帮忙做Withholding 或Sell to cover等帮忙卖股票的操作(这里区别于RSU)。

所以如果自购买日起、当年度的税务年度自己都没有主动卖出,在下一年度准备申报税务时,将不会收到跟ESPP有关的股票交易1099-B或Consolidated Tax Satements(但还是有可能因为收到股利而有Form 1099-DIV)。

3. ESPP卖出时的税务议题

ESPP也会在卖出时有两种情况:合格和非合格,Qualifying Dispositions和Disqualifying Dispositions,这两种dispositions分别有不同的税务处理方式。

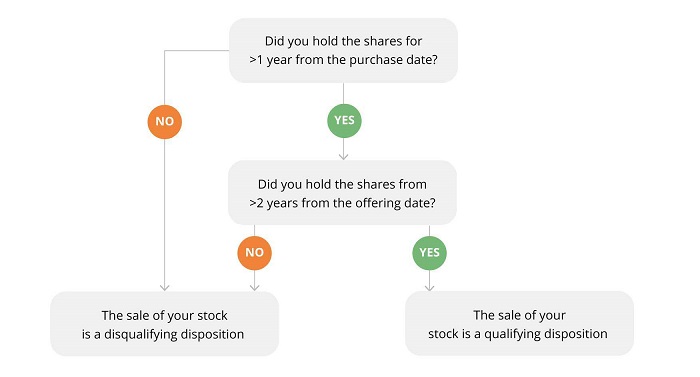

图解如何分辨合格和非合格

(1)Qualifying Dispositions

Qualifying Dispositions要符合特定的holding periods(以下两者都要符合)

Sell the stock(s) at least two years from the offering date, and

Sell the stock(s) at least one year from the purchase date.

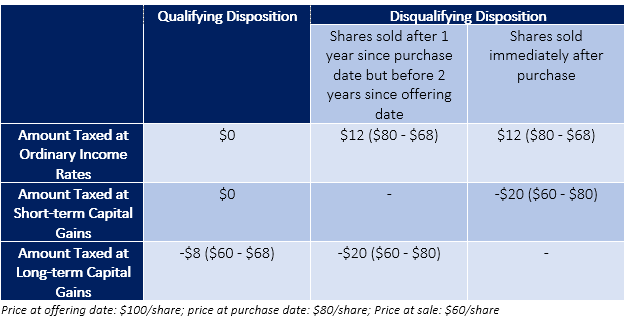

Qualifying Dispositions在认列Ordinary Income时,会以下列两者算出数值取其低者列为Ordinary Income;其它部分再列为Capital Gain/或Capital Loss的部分。

The discount offered based on the offering date price, or

The gain calculated using the actual purchase price and the final sale price.

(2)Disqualifying Dispositions

不符合上述Qualifying Dispositions的Holding period,则就是Disqualifying Dispositions。

Disqualifying Dispositions没有特别的税务认列优惠,会在卖出时有两部分组成的收入:

(FMV on the Purchase Date-Actual Purchase Price)*Shares=Ordinary Income,这一项目也常被称为‘Bargain element’,也就是要将在购买日得到的折扣算入Ordinary Income。

Selling Price-FMV on the Purchase Date=Capital Gain or Capital Loss

若以公司有提供lookback provision的状况而言,在每个purchase date时,会以offering date 跟Purchase date两个日期的FMV(Fair Market Value)作比较,取其低者再打折(以15%折扣为例)让员工购买。所以如果是Offering date的价格比Purchase date更低,所以用的购买价就会是Offering date的价格*0.85,则按照Disqualifying Dispositions的算法,Ordinary income算出金额就会比Qualifying Dispositions更多。